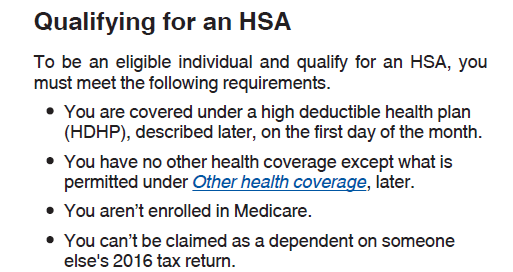

Overview

A frequent question those considering Health Savings Accounts often ask is, “What are the Pro’s and Con’s of HSA’s”? There are many different aspects of HSA’s that may benefit your particular situation, but there are some disadvantages as well. To clarify the issue, we have summarized the pro’s and con’s of Health Savings Accounts in a digestible format. Hopefully this information can help you decide if participation in HSA insurance is right for you.

There are many reasons that Health Savings Accounts are beneficial and can help your family financially. Enrolling in HSA eligible insurance and opening a Health Savings Account can offer you the following benefits:

Lower Insurance Premiums

A core tenant of High Deductible Health Plans (HDHP’s) is a trade off of lower monthly premiums in exchange for a higher deductible. This reduces guaranteed costs (premiums) at the expense of occasional costs (deductible). This benefits healthy individuals and those that can pay for limited out of pocket care.

Lower Cost of Health Care

Part of the HSA’s triple tax advantage is that qualified medical expenses are paid on a tax free basis. The actual mechanism occurs first through tax free contributions to a Health Savings Account, then spending those dollars on qualified medical expenses. By not paying tax on healthcare, you reduce your cost by your marginal tax rate, which can be 15%, 25%, or 35%.

Lower Taxes

HSA’s are an effective vehicle to lower your income tax burden. For those in strong financial standing, they can allocate part of their income to an HSA instead of paying full taxes on it, creating a nest egg and lowering that year’s taxable income.

Keep the Money Forever

Unlike Flexible Spending Accounts (FSA’s) whose contributions expire at year end (the horror!), anything you contribute to your HSA remains yours for life. There is no need to operate under a “use it or lose it mentality”. This makes an HSA an investment since it becomes savings that you can spend as you see fit.

Get Started Quickly

Unlike other health plans and savings vehicles, you can open Health Savings Account very quickly. It does not require much paperwork or employer approval; all you really need are an HDHP and an account with a financial institution. Moreover, in the first year you can utilize the Last Month Rule to contribute the max amount, even if you only had partial year insurance.

Retirement Investment Vehicle

A major benefit of HSA’s occurs when the account holder turns 65, at which point HSA funds can be spent on anything without penalty. This differs than prior to age 65, when using HSA’s for non qualified medical expenses invokes both tax and penalty. Note that HSA funds spent on non qualified medical expenses will be taxed (like a 401(k)) but not penalized. However, the benefit is they would have grown tax free in your HSA. That means you can save diligently through your working years, spend what you need on medical, and use the rest to pad your retirement account.

Unemployment Safety Net

Health insurance premiums are generally not considered a qualified medical expense. However, if you are collecting government unemployment benefits, you are allowed to spend your HSA on health insurance premiums during that time. That means your HSA can function as your own unemployment insurance and help you through difficult times after losing a job.

Employer Contributions

If you are so lucky that your employer makes contributions to employee HSA’s, you may be able to receive some of that free money by signing up an HSA. This incentive can factor into your calculation when determining what type of insurance to buy.

The Con’s of HSA’s

Even though there are many positive aspects of HSA’s, there are some Con’s as well. Generally these involve the insurance itself and the IRS rules surrounding the account mechanics. Either way, it is important that you are aware of the following when making a decision about HSA’s.

Reduced Insurance Choices

Since not all insurance plans are HSA eligible, if you want an HSA you will be restricted to a subset of health insurance plans. These plans may or may not fit all of your health care needs, so be sure that your needs are being met by the insurance. In that regard HSA eligibility may be a “bonus” or a secondary factor in deciding which insurance to purchase.

Higher Deductible

The increased deductible required by HDHP’s is a reality that can cause financial hardship. It is not fun to have to spend $X,000 before your insurance kicks in, and the higher the number, the more you spend first. That is why if you have high medical costs an HDHP may not be the best fit for you.

Money tied up for Health Care

One downside of HSA contributions is that they are illiquid. Once they have been contributed, they are designated for medical expenses and nothing else. This can cause financial issues when you have a bunch of money in your HSA but have a non-medical need for the cash. There are a few ways to cash out an HSA but they often involve taxes and penalty.

Risk of Penalty and Fines

There are quite a few rules that govern the use of HSA’s, and some of them are very specific and (dare I say) onerous. By using an HSA you receive benefits but run the risk of putting yourself in a position to actually pay penalties if something goes wrong. The most common cause of fines is the Last Month Rule, so it is in your interest to familiarize yourself with it and other HSA rules.

————————————

Note: if you have an HSA, please consider using my service EasyForm8889.com to complete Form 8889. It is fast and painless, no matter how complicated your HSA situation may be.