This question was submitted by HSA Edge reader Steve. Feel free to send in your question today to evan@hsaedge.com.

I will be age 55 on 12/4/18 and have single-person HSA coverage. Must I wait until I am actually 55 in December to make the $1,000 extra contribution, or can I begin making monthly contributions now and throughout the rest of 2018 that total an extra $1,000? My employer won’t allow extra contributions until I am actually 55 on 12/4/18.

Making an HSA 55+ Catch Up Contribution

Health Savings Accounts have a great feature for those 55 and older that allows you to contribute an additional amount each year, currently set at $1,000. This extra amount is added to your self-only or family contribution limit, which allows you to contribute your self only or family amount, plus the additional $1,000 each year. We like this because it lets you contribute more money to your HSA. Now, this assumes that you did not end coverage during the year, in which case the self-only and catch up contribution are pro-rated for the months you had coverage. Either way, it is a great way to get some extra funds into your HSA.

The question at hand is one of timing. Can you make the 55+ contribution any time during the year you turn 55? Or, if you are not yet 55, do you need to wait until your 55th birthday to actually make the 55+ contribution? If the latter was the case, that leaves Steve with only 2 weeks before the end of the year to make that contribution. Moreover, his employer is telling him he needs to wait until this time to make the contribution. How do they track and enforce that? For example, if I am contributing 1/12 of my limit per year, including the $1000, I am “under” contributed for about the first 10 months of the year.

55+ Contribution Can Be Made Anytime During Year

Luckily, the IRS opines on this matter indirectly in Form 969 and it is favoriable to the consumer:

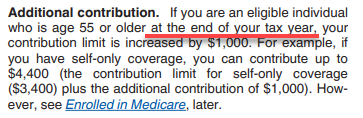

Here, the IRS states that the eligible individual who is 55 or older by the end of the tax year has their contribution limit increased. Remember that HSA contribution limits are per year, so you only have 1 contribution limit for a given year. Generally, you can determine that limit on January 1st (barring any change in coverage). Contrary to what Steve’s employer states, the IRS does not say that the catch up contribution limit is only increased pro rata by age, or only applies once the person actually turns 55, or can only be contributed to once the person is 55. It simply states that if you will be 55 during the calendar year, your contribution limit is increased. Thus, the reality is you can make that contribution whenever you see fit.

In Steve’s case, he will be 55 in December at the end of 2018. Thus, his 2018 contribution limit is increased for the entire year. That means that he can begin contributing his 55+ contribution as early as January 1st, 2018. He does not need to wait until he is actually 55 to make that catch up contribution.

I advised Steve to take this up with his employer and HSA custodian. While an employer can create any rules they wish, this is likely a simple oversight of how HSA plans function. Hopefully they can change this to align with how HSA’s work and make it easy on people like Steve who have late birthdays. It also allows people to gain the benefits of front loading their HSA contributions early in the year.

Note: if you need help accounting for your 55+ contributions on your HSA taxes, please consider using my service EasyForm8889.com to complete Form 8889. It is fast and painless, no matter how complicated your HSA situation.

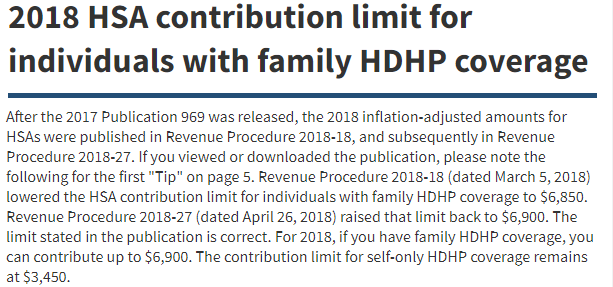

[Update May 2018: note that as of April 26th, 2018, the IRS has reversed course and reset the 2018 Family HSA limit to $6,900. This was the original amount that was decreased to $6,850 in March. See below for information on the decrease, and read on to hear the fury and toil it caused.]

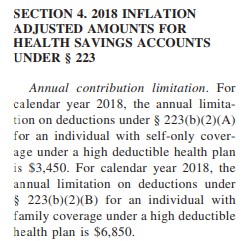

Not in our wildest dreams did we consider this possible: the IRS has lowered the 2018 HSA Family Contribution Limit two and a half months into the tax year. Yes, you read that correctly. Previously, the 2018 Family Contribution limit for Health Savings Accounts was $6,900, and due to an inflation calculation change, this has been reduced by $50 to $6,850 as of March 5th, 2018. Fortunately, self-only and catch up contribution rates were unchanged.

Only the 2018 Family contribution limit has been affected, and while the inflation calculation may alter the course of future contribution limit increases, only 2018 is in play as we are mid year. It is not immediately clear what the total impact is for this change in contribution limit mid year. Obviously, HSA eligible individuals on family coverage will not be able to contribute as much this year. Here are the likely impacted parties:

Family coverage that already contributed max – there are some “all star” HSA users that are fortunate enough to make full year HSA contributions at the beginning of the year. They often do this to get their money invested in the market to receive a return on their funds for the year. Those people (retroactively) have an excess contribution of $50 that they need to remove. It would be easiest to do this ASAP to avoid interest / gains on that money needding to be calculated and removed. Easy, no penalty process but an annoyance for $50 when you did everything right.

Family coverage planning on contributing the max – if you set your 2018 contribution to $6,900 but haven’t fully contributed that amount yet, you are likely in good shape. Most HSA custodians will prevent you from making an excess contribution against the plan limits. When they update their plan limits, this equation will kick in, and likely prevent a problem once you get to $6,850 in contributed funds sometime this year (depending on your monthly contribution amount).

IRS – the IRS will need to update all of their data regarding this maximum deductible amount for 2018. Obviously, they didn’t see this as a big issue as they proceeded with the change mid year.

HSA Plan Custodians and Insurance companies – there is much work to be done by HSA custodians and insurance companies. Every single custodian and plan that administers HSA’s is now out of whack, thanks to a minor $50 change. All of their programs, banking software, websites, and literature needs to be updated. This will need to be corrected, and the sum effort (and cost) for all of these entities is massive.

HSA websites – same goes for everyone sharing and publishing information about HSA’s. All of the previously published information is out of date and needs to be updated.

I will leave it to our fine readers to decide for themselves whether this mid year change for $50 was value added, intelligent, or warranted.

Why the IRS reduced the 2018 HSA Family limit

As part of the Trump tax cuts, legislation was passed that changes how inflation increases are calculated. In essence this is a net negative as the traditional CPI has been replaced with the “chained” CPI, which is different as it allows substitutions of products in the CPI basket of goods. This “substitution” effect is a classic economist assumption that means that if beef prices are rising, consumers avoid it and buy chicken instead. Beef is thus less represented in the index, meaning that total inflation is shown as lower than using the regular CPI. This will result in lower cost of living increases across the board going forward. While this is a negative, the real mistake was implementing it for 2018, and not waiting for a fresh tax year.

For those following along at home, here is the text on the section changing the CPI calculation:

.03 Section 11002 of the Act amends § 1f(3) to provide a permanent cost-of living adjustment based on the Chained Consumer Price Index for All Urban Consumers (C-CPI-U). Any existing items that are not reset for 2018 will be adjusted for inflation after 2017 based on the C-CPI-U. Items that are reset for 2018 will be adjusted for inflation after 2018 based on the C-CPI-U

All in all, a moderate sized change that creates a lot more work for many.

If you made contributions to or distributions from your HSA in 2017, you will need to file the federal tax form 8889. This form is specific to HSA’s and records all activity with your HSA for the year. It flows to Form 1040 to adjust your income: your contributions reduce your taxable income, whereas any penalties adds back to income, increasing tax.

Form 8889 is not as straightforward as it could be, so I created a service called EasyForm8889.com that completes your form for you. I have also created the following video to walk through how to file Form 8889. Little has changed since the 2016 form used in this video. Check it out, otherwise, the transcription of the information is below.

The 2017 HSA tax form presents little difference to prior year tax forms. Throughout the form you will see the tax year incremented to 2017, so make sure you are working on the correct version. This can be confirmed in the upper right of the form. Contribution limits have increased in 2017, so these amounts are reflected throughout the form (specifically Line 3).

The 2017 Form 8889 instructions have been released by the IRS and can be found here. They are substantially the same as prior years save for year and contribution limit updates.

2017 HSA Contribution Limits

For self-only coverage, the maximum contribution limit increased by $50 to $3,400 in 2017. There were no changes to the family coverage amount which is $6,750, as well as the 55+ catch up contribution amount of $1,000. The IRS defines the maximum amounts that may be contributed to a Health Savings Account each year. Per IRS Publication 969:

The amount you or any other person can contribute to your HSA depends on the type of HDHP coverage you have, your age, the date you became an eligible individual, and the date you cease to be an eligible individual…for 2017, if you have self-only HDHP coverage, you can contribute up to $3,400. If you have family HDHP coverage you can contribute up to $6,750.

Here are HSA contribution limits for prior years:

2014

2015

2016

2017

Self-Only HSA Contribution Limit

$3,300

$3,350

$3,350

$3,400

Family HSA Contribution Limit

$6,550

$6,650

$6,750

$6,750

55+ Additional Contribution Limit

+$1,000

+$1,000

+$1,000

+$1,000

The maximum contribution amount for your HSA in 2017 is $3,400 for self-only coverage and $6,750 for family. Note that this does not include the additional 55+ catch up contribution of $1,000 allowed to properly aged HSA holders. Thus, if you are over 55 on or before the end of 2017, you can contribute $4,400 for self-only coverage or $7,750 for family coverage.

2017 HDHP Definitions

To qualify as an HDHP, your health plan cannot exceed an out-of-pocket maximum limit established by the IRS. There were no changes to these amounts from 2016 to 2017. For self-only plans, the minimum deductible remains $1,300 and the out of pocket maximum is $6,550. For Family plans, the minimum deductible is $2,600 while the out of pocket maximum is $13,100. Plans with a deductible below that specified are not HSA eligible, nor are plans with an out-of-pocket max greater than those listed. The HDHP definitions for recent years are summarized below:

2014

2015

2016

2017

Self-Only Min Deductible

$1,250

$1,300

$1,300

$1,300

Self-Only OOP Max

$6,350

$6,450

$6,550

$6,550

Family Min Deductible

$2,500

$2,600

$2,600

$2,600

Family OOP max

$12,700

$12,900

$13,100

$13,100

2017 HSA Form 8889 example

Let’s walk through an example of the 2017 Form 8889 to show how it works.

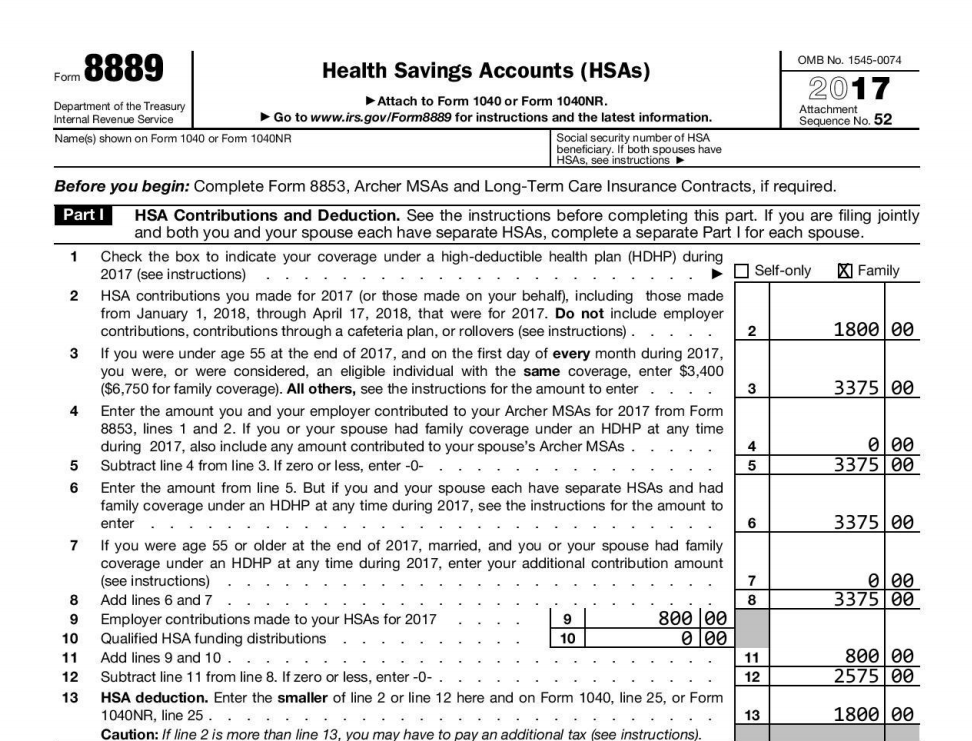

Let’s assume I am a married 40 year old who had family HSA eligible coverage from January – June of 2017 (6 months). On July 1st, I changed to a non-HSA eligible plan. My spouse does not have their own Health Savings Account. I contributed $1,800 to my HSA and my employer contributed $800. I distributed $800 from the HSA during the year, all of which I spent on qualified medical expenses.

Part I – Contributions and Deduction

Form 8889 starts off pretty simply on Line 1 by asking the type of insurance you had (mostly) during the year. For this example, it is family. Line 2 then goes on to ask how much you contributed to your HSA during the year. In our case this was $1,800, which does not include employer contributions. Line 3 can be quite complicated, but in essence you need to list your contribution limit for the year. If you had self-only or family coverage all year, the amounts are provided for you. Otherwise, you need to prorate your coverage by month. In this case, we had family coverage for 6 months, so our contribution limit is $3,375 for 2017. Line 4 asks about Archer MSA’s (does not apply here) and Line 5 is a simple subtraction.

[Note: all 2017 tax forms were generated in minutes using EasyForm8889.com]

We continue with Line 6, which for self-only filers equals Line 5. For family coverage where both spouses have their own Health Savings Account, each of you needs to file your own Form 8889. Then on Line 6, you allocate the share of the contribution limit that belongs to that HSA. In this case, only the insured has an HSA, so this line equals Line 5. For some situations, Line 7 adds the $1,000 catch up contribution, but our example assumes the HSA holder is 40 years old so this does not apply. Line 8 is simple subtraction, and the $800 employer contribution comes into play on Line 9. If you contributed to your HSA from an IRA you would indicate that on Line 10, and Line 11 is simple addition. Line 12 is subtraction, and Line 13 does a comparison to calculate what your 2017 HSA deduction is, which makes its way to Form 1040. In our case, it is the $1,800 we contributed to the HSA.

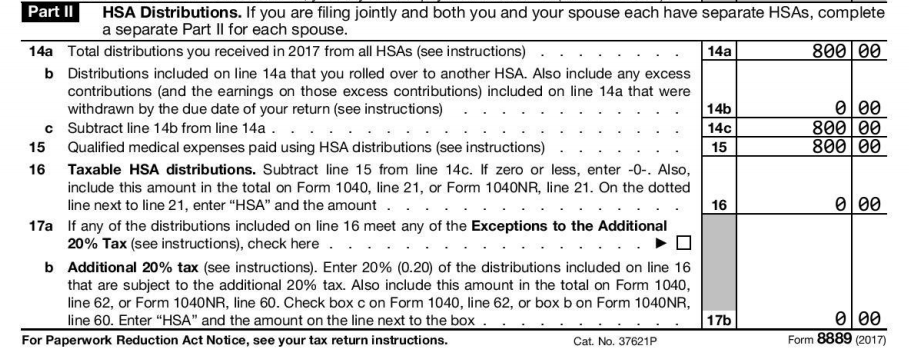

Part II – Distributions

The second part of the 2017 Form 8889 deals with distributions, or amounts that came out of your HSA. We assume that we distributed $800 from the HSA, so that amount is shown on Line 14a. Line 14b lists rollover amounts and excess contributions that were removed, and Line 14c subtracts them out. The filer tracked his qualified medical expenses and receipts using TrackHSA.com this year, so he can easily prove all $800 in distributions were used for medical expenses. He places that amount in Line 15. A subtraction occurs on Line 16 to determine any amounts not spent on qualified medical expenses; luckily that is $0 for us. If you had an amount on Line 16, Line 17a gives you the chance to exclude this from taxation based on a few exceptions. Otherwise, that Line 16 amount is taxed 20% on Line 17b, which gets recorded on Form 1040.

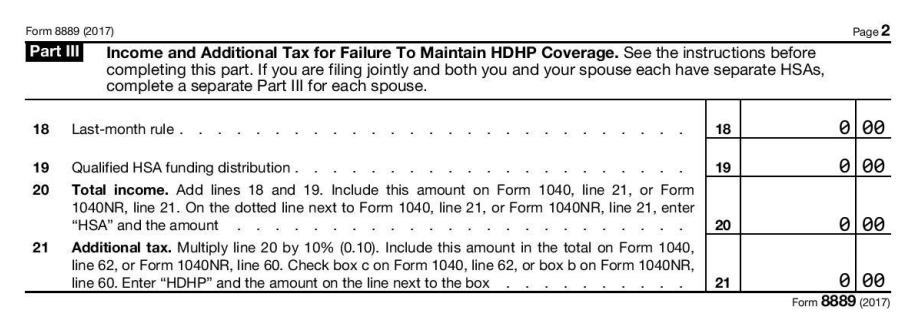

Part III – Penalties and Taxes

For most people, Part III will look a lot below: all zeroes. This is good, but it is possible that you have accrued some taxes and penalties. If in the prior tax year, you 1) used the Last Month Rule and proceeded to 2) fail its Testing Period, a difficult calculation awaits you on Line 18. You are going to have to go back, figure out how much you contributed in the prior year, redetermine what you could have contributed without the Last Month Rule, and place the difference here. On a similar note, if you made a qualified funding distribution from your IRA but failed its Testing Period in 2017, you will have to enter the amount that failed in Line 19. Once that is done, Line 20 adds Line 18 and Line 19 and adds it back to income (where it is taxed) on Form 1040. Finally, for good measure, Line 21 assesses a 10% penalty against the amount on Line 20, which also makes its way to Form 1040.

Note: if you need help with your 2017 Form 8889, or just want it done right now, please consider using my service EasyForm8889.com. It asks simple questions in a straightforward way and will generate your completed HSA tax forms in 10 minutes. It is fast and painless, no matter how complicated your HSA situation.